Commercial and Industrial (C&I) loans give lenders the opportunity to generate greater interest income compared to commercial real estate loans. There aren’t as many banks competing for these types of loans, and community banks with the right expertise can have a real competitive advantage over larger banks because they have deeper relationships with the local business community.

So why aren't more community banks pursuing C&I loans?

Many community banks are overlooking the potential in C&I loans. They believe that commercial real estate loans are safer because they have better collateral. During the recent recession, this belief was proven quite wrong. And yet, for many lenders, the behavior didn’t change – even as the economy improved and real estate developers expected lower and lower interest rates.

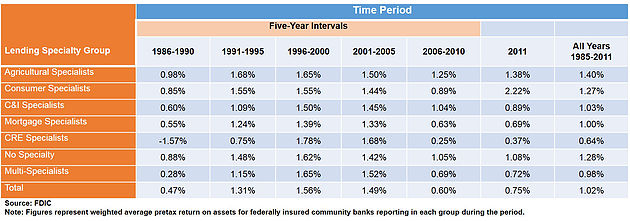

In the FDIC’s detailed look at comparative performance of community bank lending specialty groups in 2012, the banks that focused on commercial real estate performed the worst during the study’s 26-year period.

What makes a loan sound is sufficient cash flow. At LendXP, we’ve worked with many community banks to structure C&I loans. Using the SBA and USDA not only allow lenders to safely provide needed funds to local businesses, but generate high noninterest income when they sell the guaranteed portion of the loan, bringing future interest income into the current year. Surprisingly, C&I loans to companies with insufficient collateral to support the loan allow even greater opportunities for increased profitability without undue risk.

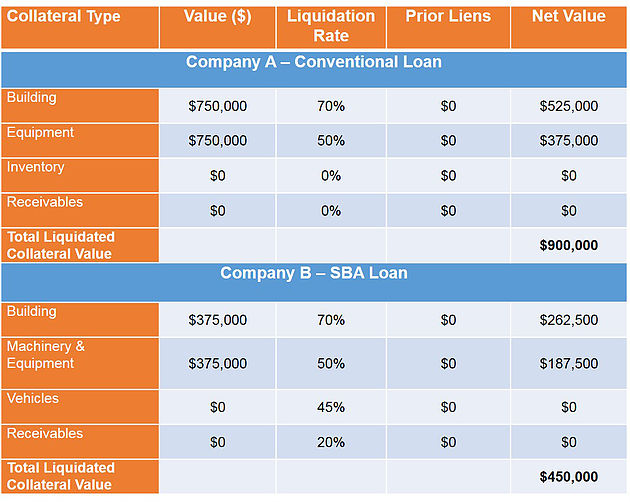

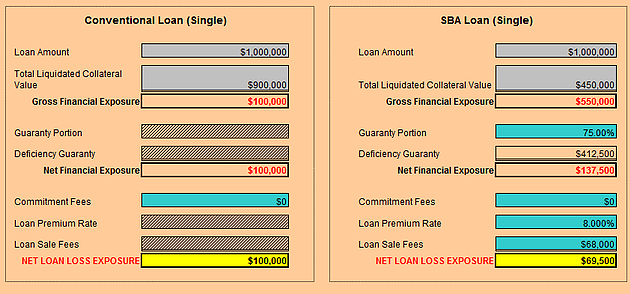

Let me show you an example featuring two different companies: Company A and Company B. Company A and Company B both want a $1 million dollar loan. Company A has 150% collateral coverage for the loan amount. Company B has 75% collateral coverage for the loan amount. Would you believe that the net loan loss exposure for Company B is actually less when using an SBA guarantee?

First, let's review the collateral for Company A and Company B. Company A has sufficient collateral and qualifies for a conventional loan. Company B has insufficient collateral to qualify for a conventional loan and uses an SBA guarantee.

Now, let's look at how to utilize a government guarantee through programs such as the SBA 7(a) loan program to manage risk.

Interested in learning more? Community banks throughout the Midwest are improving performance and managing risk by partnering with LendXP. View our services.