In December of 2012, the FDIC completed a Community Banking Study in an effort to identify issues and explore questions about community banks in comparison to non-community banks. A common measure for comparing the financial performance of banks of different sizes is evaluating the pretax return on assets (ROA). A comparison of pretax ROA reveals that during the 27-year FDIC study period (1984-2011), non-community banks outperformed community banks. The pretax ROA for non-community banks averaged 1.31% while community banks averaged 1.02% over the study period. The difference in performance was due almost entirely to the fact non-community banks generated more non-interest income from a wider variety of sources than community banks. In today’s banking climate, cbe sold on the secondary community banks have found it possible to grow and prosper not by trying to emulate large banks, but rather, by performing largely traditional functions with more efficiency.

One way for community banks to close the all-important noninterest income gap can be found in a traditional lending function – lending to small businesses. Loans made to eligible small businesses can be backed by loan guarantees from the U.S. Small Business Administration (SBA) and the U.S. Department of Agriculture (USDA). The guarantees can then be sold on the secondary market, generating significant noninterest income. Additionally, this allows the lender to retain the unguaranteed portion of the loans on their books, generating additional interest income for the bank.

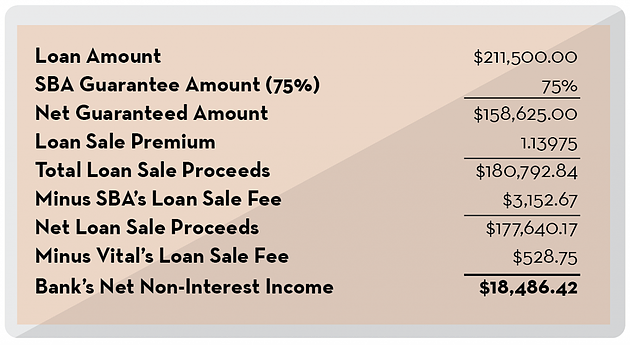

To demonstrate the amount of non-interest income a community bank can make on an SBA loan, LendXP recently partnered with a community bank to make a $211,500 loan to an eligible small business. SBA guaranteed 75% of the loan. The loan was sold on the secondary market at a 113.975 premium.

| Loan Amount | $211,500 |

| SBA Guarantee Amount (75%) | 75% |

| Net Guaranteed Amount | $158,625 |

| Loan Sale Premium | 1.13975 |

| Total Loan Sale Proceeds | $180,792.84 |

| Minus SBA'a Loan Sale Fee | $3,152.67 |

| New Loan Sale Proceeds | $177,640.17 |

| Minus LendXP's Loan Sale Fee | $528.75 |

| Bank's Net Non-Interest Income | $18.486.42 |

Therefore a $211,500 SBA loan generated net non-interest income of $18,486.42. A $1,000,000 loan has the potential to generate non-interest income in the $90,000 range, depending on current loan sale premiums. Selling a USDA loan on the secondary market can generate similar loan sale premiums. By utilizing the SBA and USDA and taking advantage of selling the guaranteed portion of a loan on the secondary market, community banks can perform a traditional function – lending to local farms and businesses – and effectively close the noninterest income gap with noncommunity banks to significantly increase their return on average assets.

Are you ready for your community bank to perform at higher levels? Give the team at LendXP a call at (515) 850-1567 to discuss how noninterest income can bring the ROA of your community bank to levels rivaling those of larger banks!