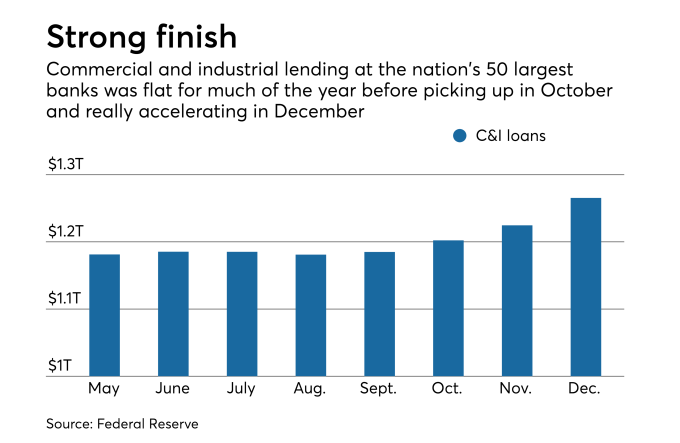

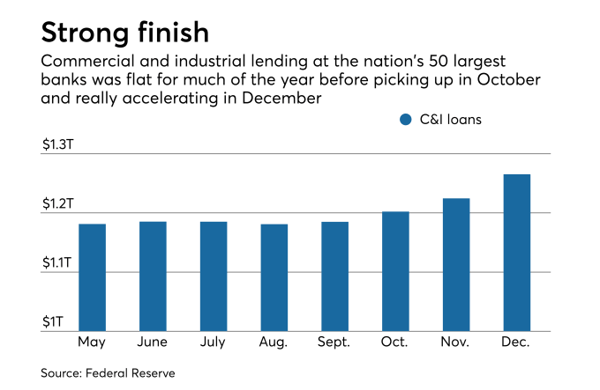

Chart from American Banker.

According to this article, bankers and analysts are optimistic about C&I lending in 2019. The strong uptick in C&I loan demand at the end of 2018 is expected to continue this year. We’re seeing it at LendXP, and are connecting interested lenders with new C&I loan opportunities.

So how can your bank participate in the trend if C&I lending isn’t your strong suit? Here’s our recommended approach.

1. Strategically use SBA Guarantees

Common reasons why a C&I business may not fit the criteria for a conventional loan include a lack of collateral or seasonal or cyclical business revenues. Don’t let the conversation end there! Businesses with good cash flow may be eligible for an SBA which mitigates additional risk by providing lenders a guarantee of 75-90% of the loan amount. There are additional benefits for the borrower too, such as longer terms and better interest rates than alternative or nonbank financing.

(Not familiar with the SBA loan process? No problem – LendXP will provide support from origination until the last payment is made.

C&I business customers also have other banking needs beyond loans, such as depository services, treasury management, credit cards, and insurance. This creates a positive ripple effect throughout service areas of the bank.

2. Leverage the secondary market.

There is a strong and active secondary market for loans backed by the SBA. Lenders can sell the guaranteed portion of the loan, generating noninterest income and increasing liquidity, allowing lenders to continue making loans. This is a particularly beneficial strategy for banks with high loan-to-deposit ratios.

Factors such as term, spread, and interest rate adjustment period will impact the premium lenders receive. For those that want to participate in secondary market sales, LendXP will provide guidance on the structure of the loan and facilitate the sale.

3. Proactively manage credits.

Companies are living, breathing entities that experience an ongoing change in the factors that impact performance. A good best practice is to collect data annually from your C&I customers, such as financial statements and tax returns.

If you notice a customer is starting to become late on payments, don’t wait until the problem becomes chronic! Check-in with your borrower at the first signs of distress. There are robust analysis tools that can help you get a better picture of the financial health of your borrower. We’ve written here about a tool we use at LendXP. When you work with us, we’ll provide guidance and tools that support you in managing your C&I credits.

4. Pick the right partner.

If your bank is currently focused on commercial real estate loans, we understand that you’re not going to become a C&I lending bank overnight.

But, over-concentration is risky, and diversifying your portfolio with C&I loans is a smart strategy to begin implementing now. LendXP is highly experienced in financing C&I businesses and can provide the support you need if C&I loans are outside of your comfort zone. We’ll help you source opportunities, navigate SBA underwriting, close, sell and service loans.